When Risk Moves, Not Disappears

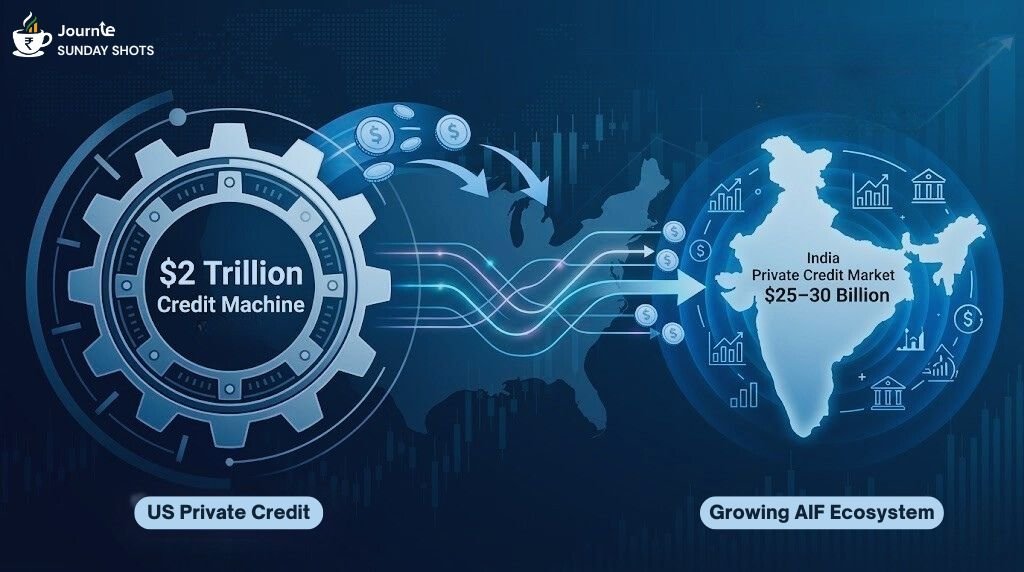

Private credit emerged after the financial crisis to fill the lending gap left by banks. And in many ways, it succeeded.

But as the market has expanded, the lines between traditional banking and shadow lending are beginning to blur again.If stress appears, it may not resemble the banking crises of the past. There may be no sudden bank runs or dramatic collapses.

Instead, the signals could be quieter. Slower fundraising. Tighter liquidity. Harder refinancing cycles.

And that is why developments in the U.S. private credit market are being watched more closely. Because in modern finance, capital rarely stays confined to one market.

Sometimes the first signals appear far away, long before the ripple reaches everyone else.Until next Sunday!