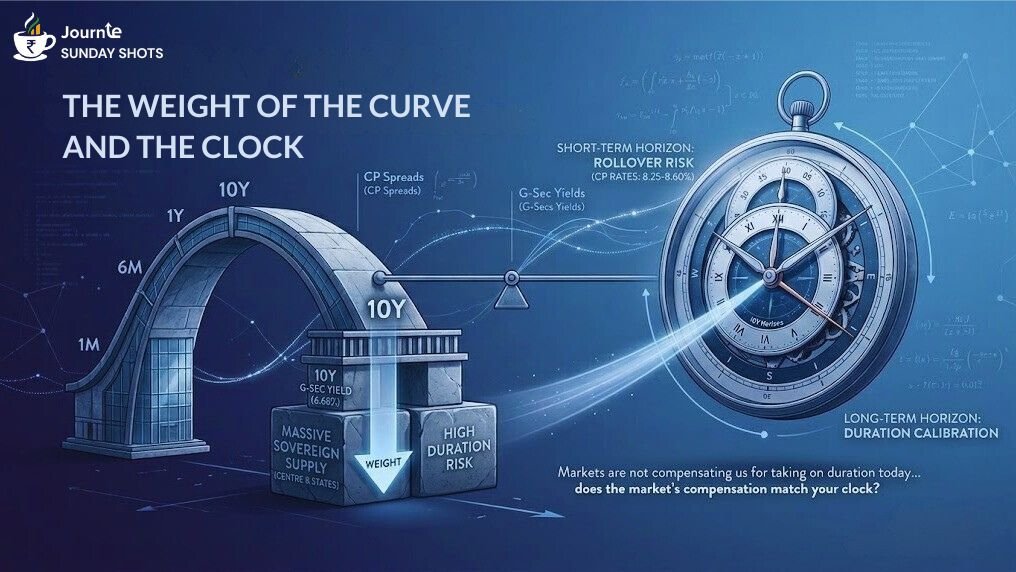

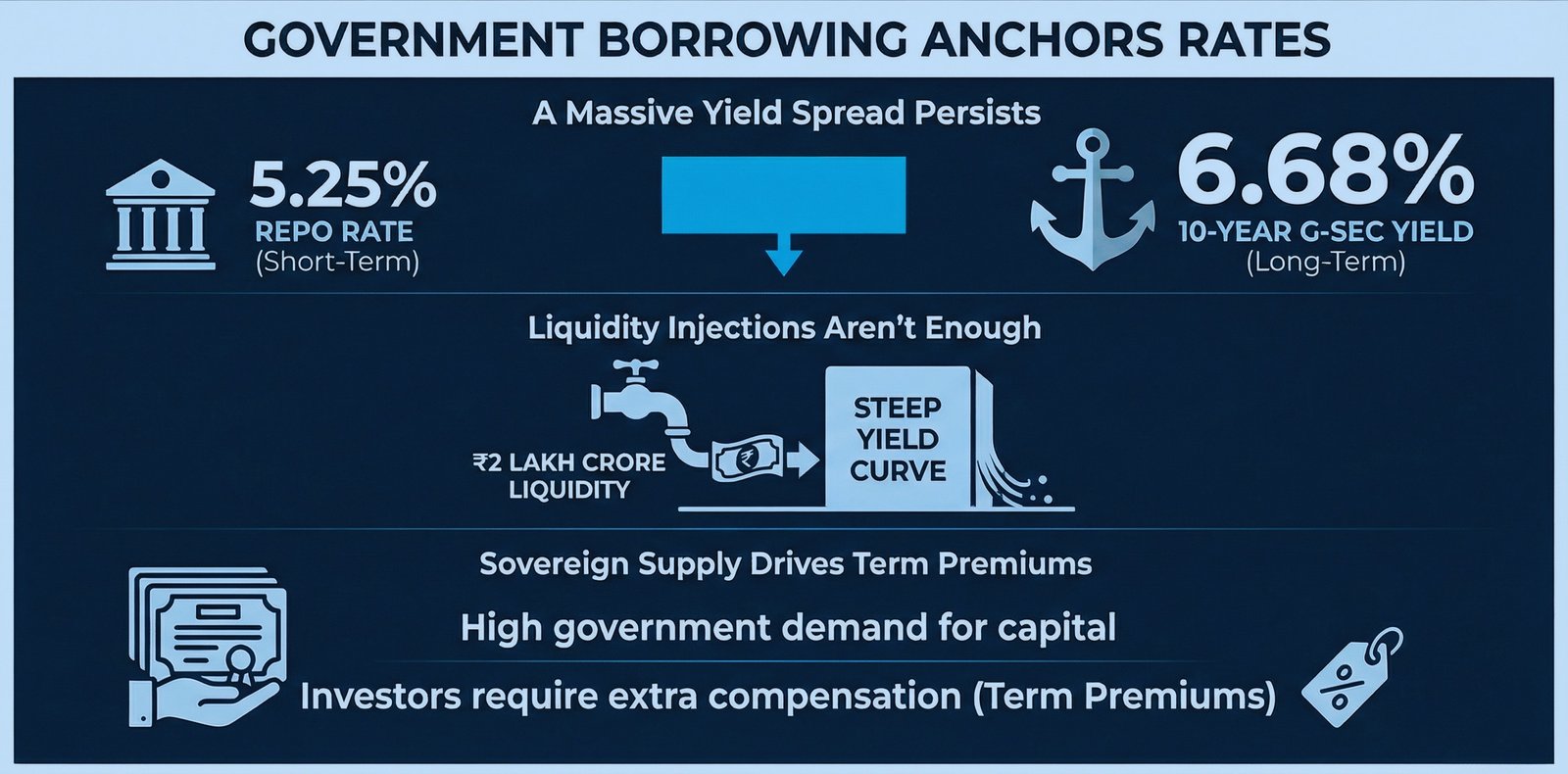

Finding the Right Bucket

The real task for a treasury team today isn’t to constantly hunt for the highest-yielding bucket. It is to make sure you are standing in the right bucket when the next risk repricing happens.

Markets are not compensating us for taking on duration today, but visible carry without invisible duration risk is exceptionally rare.

Static yield chasing works perfectly—right up until the moment policy action, sovereign supply pressure, and bank funding conditions intersect. Because when the curve steepens, timing matters as much as price.

The question is: does the market's compensation match your clock?

Until next Sunday!