The Sorting Investor & The Hidden Cost of Recency

Ever opened an investing app, sorted by “1-year returns,” and felt that sense of satisfaction picking the fund at the top?

That feeling is familiar. It’s human. And it’s where things start going wrong.

Recently, Radhika Gupta, CEO of Edelweiss Mutual Fund, put a name to this behaviour: “The Sorting Investor.”

It landed because it described something most investors do, often without realizing it.

They don’t speculate. They don’t gamble. They don’t chase tips.

They simply sort and choose – by returns, by rankings, by whatever sits at the top

Clean. Logical. Efficient. It feels like how smart people should invest.

The data, however, tells a very different story.Meet the Sorting Investor

Imagine Raj. He’s a CFO — sharp, analytical, careful with money. He has ₹50 lakh of surplus cash to deploy.

On a Sunday evening, he opens his investment app and sorts equity funds by last year’s returns.

A Mid cap fund stands out — up nearly 38%. Clean chart. Top rank. Easy decision.

Raj invests. And three months later, market leadership shifts. Large caps gained strength as midcaps cooled off. The fund slips down the rankings.

Raj switches. Buying high, selling low, without realizing it.

Nothing reckless. Nothing emotional. Just one reasonable decision after another.

How Sorting Became the Default

This wasn’t always the norm.

Sorting investors didn’t emerge because people became careless. They emerged because information became abundant and interfaces trained their behaviour.

Today, every platform leads with performance tables, media headlines celebrate annual winners and fund factsheets open with recent returns

Over time, a simple idea gets reinforced: The best fund is the one that did best recently.

So, investors optimize for visibility, not durability.

What the Data Actually Says

- Funds at the top of rankings frequently fell sharply the following year

- Many slipped into the bottom of the performance

- Even over three-year windows, leadership changed frequently

- Only a small fraction of top-ranked funds repeated their performance

| From Top Rank | Next Year Reality |

| #1 Funds | 80% drop to mid/bottom |

| Top 10 | Only 20% repeat |

The Illusion of Intelligence

Sorting feels analytical. But notice what usually gets ignored:

- How did this fund behave during stress?

- How wide are its outcomes?

How often does it beat its benchmark? Instead, the question becomes: “Who looked smartest last year?”

That’s not investing. That’s pattern-chasing.

Sorting by recent returns assumes continuity. Markets specialize in breaking it.

Recency bias makes investors think recent winners are safer bets despite no statistical evidence.

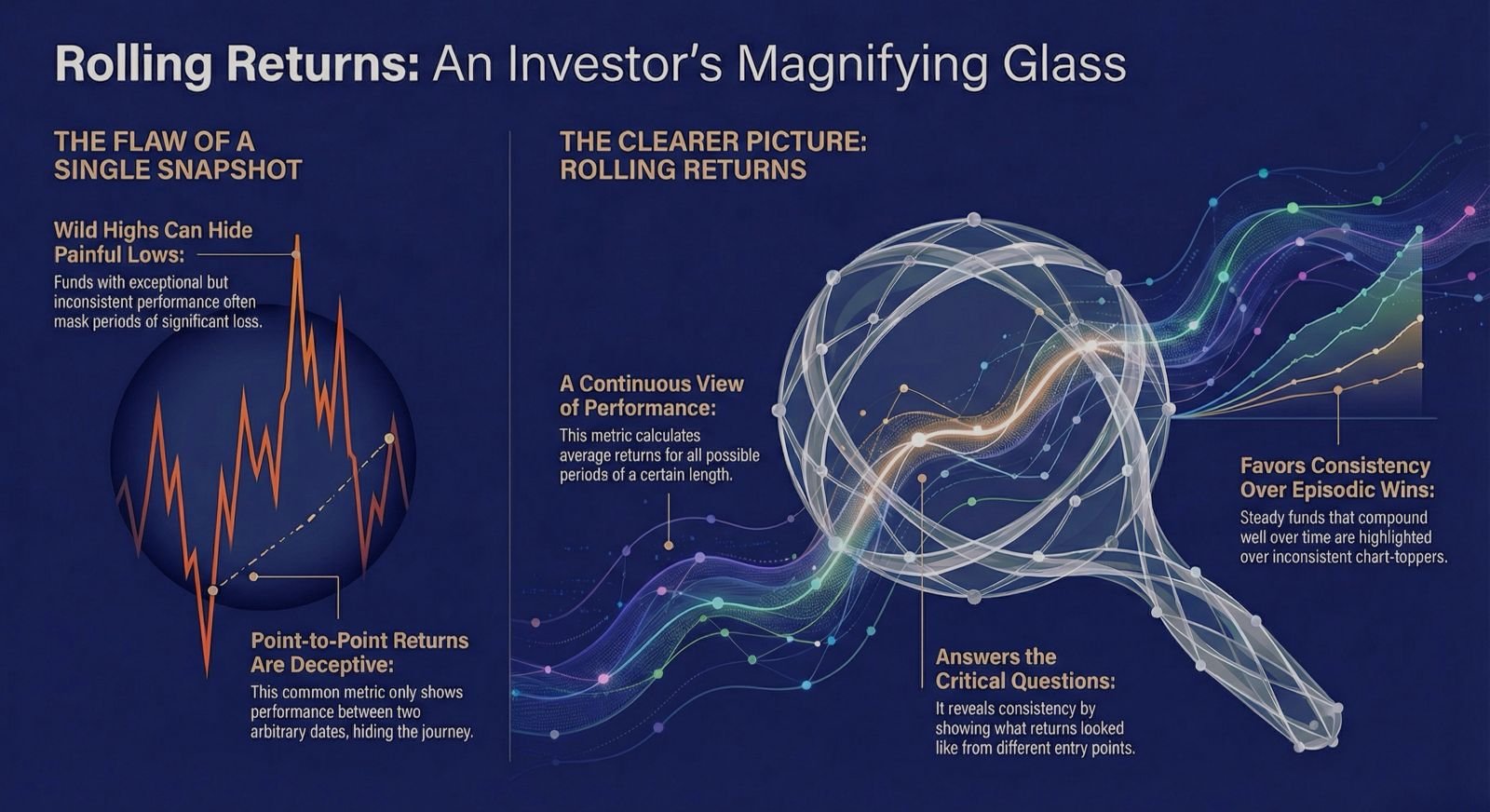

The Metric That Changes the Conversation

This is where the lens changes.

Rolling Returns – A favourite metric of Experienced investors.

Instead of point-to-point returns, Rolling Returns is a better way to understand the performance of a fund. It answers the uncomfortable questions like:

- What did returns look like across different entry points?

- How bad did the worst periods get?

- Was the performance consistent, or episodic?

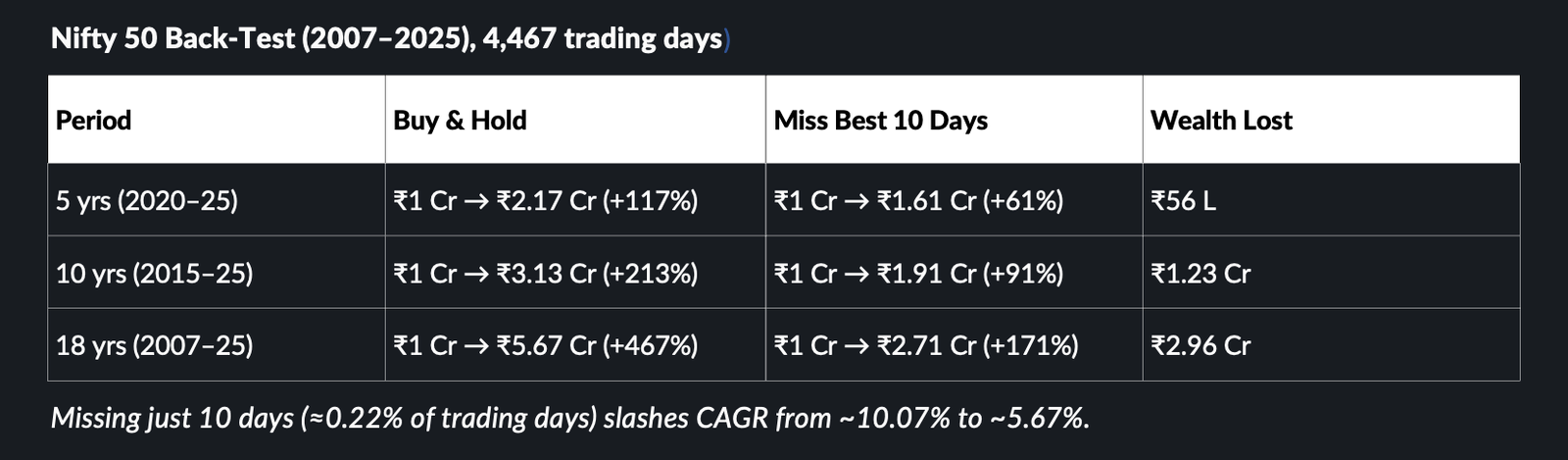

Rolling Returns explain the performance of funds, not by one good year, but by consistency across many imperfect ones.

Funds with wild highs often hide painful lows. Steady ones rarely top leaderboards but compound better over time.

The Consistency Problem

Here’s where the story gets harder.

Across markets, a majority of actively managed funds struggle to beat their own benchmarks over extended periods. In fact, scorecards published by S&P Dow Jones Indices repeatedly show that roughly two-thirds of active equity funds underperform their benchmarks over longer horizons.

Now, this isn’t a judgement on fund managers. It simply reflects how difficult consistency can be over long periods.

Which is why, at Journie, our approach leans toward index-based portfolios and/or optimal asset allocation — reducing fund-manager bias, anchoring portfolios to a defined investment philosophy, and evaluating the outcome over 3, 5 and 10-year rolling periods, not headline returns.

It’s less about chasing skill, and more about structuring behaviour.

The Hidden Cost of Sorting

The real cost of being a sorting investor doesn’t show up immediately.

It’s gradual and shows up over time as:

- Entering after strong runs

- Exiting during inevitable underperformance

- Constant portfolio churn

- And broken compounding

- Higher tax cost

The portfolio moves. The wealth doesn’t.

From Sorting to Staying: The Investor Shift

We’re in a phase of sharp market rotations and uneven leadership.

This is exactly when sorting behaviour peaks and exactly when it does the most harm.

Thoughtful investors don’t stop using data. They stop letting data rush them.

They don’t try to predict which fund will win next year. They choose funds whose behaviour they understand, and then give them time.

Leaderboards create movement. Processes create wealth.

And the difference between the two is usually visible only in hindsight.

Until Next Sunday!

Disclaimer: This update is for informational purposes only. Please consult a SEBI-registered advisor before investing.