The Great Salary Reset: India’s 8th Pay Commission and the Next Income Cycle

As 2026 unfolds, imagine millions of households of government employees unwrapping not just resolutions, but fatter paychecks that could light up India’s economy like Diwali fireworks.

But before we begin, we wish you and your family a Happy New Year.

May the year ahead bring health, happiness, and the quiet comfort of time well spent with those who matter most.

We start the year with an important story unfolding across India’s economy: the 8th Pay Commission — a once-in-a-decade income reset that shapes incomes, consumption, and broader economic momentum.

A Significant Reset, Not Just a Raise

Once every ten years, the Indian government hits the reset button, undertaking a comprehensive overhaul of salaries and pensions for its employees through a Pay Commission. This isn’t a marginal adjustment. It’s a structural reworking of how the Centre compensates its workforce.

The 8th Pay Commission formally comes into effect from January 1, 2026. That doesn’t mean revised salaries show up immediately. Recommendations, approvals, and implementations roll out over the year — but the framework is now live.

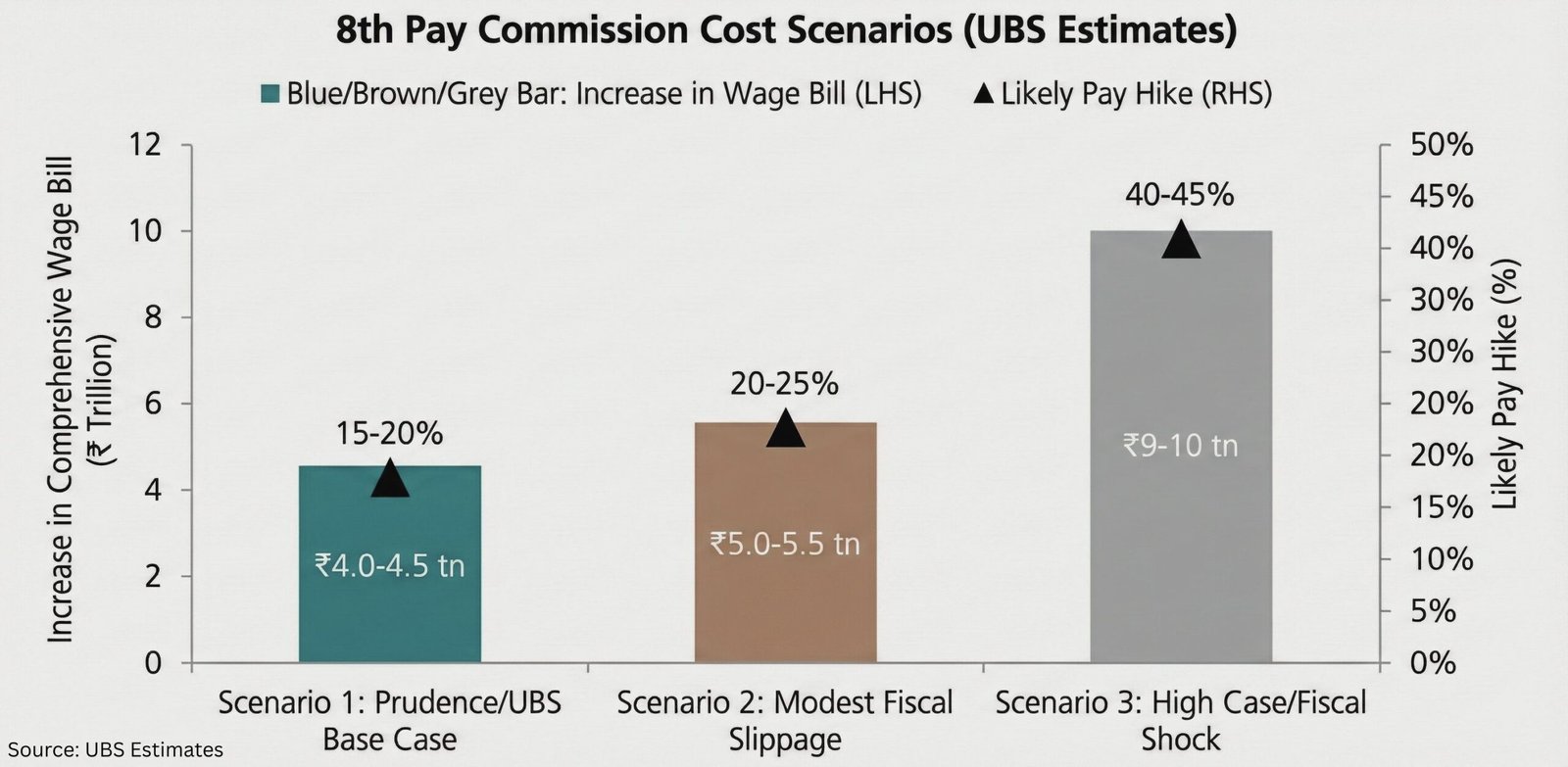

And this matters, as the scale is massive. Around 5 million central government employees and 6.5–7 million pensioners could see their pay and retirement benefits meaningfully recalibrated over this cycle. External estimates place the fiscal cost near ₹3-4.5 trillion, roughly 0.6-1.1% of GDP, spread across the implementation period.

While the recommendations apply to the Centre, state governments and public sector undertakings often align their pay structures over time, extending the impact well beyond the central payroll.

Taken together, this suggests that close to 30 million employees across government and allied entities, representing roughly 5% of India’s working population, could be directly influenced by this income reset.

Fitment Factor: The Multiplier That Shapes Outcomes

At the heart of this reset sits a single variable: the fitment factor.

In simple terms, it works like this:

Old Basic Pay × Fitment Factor = New Basic Pay

The mechanics are straightforward. The implications are not. Even small changes in this multiplier translate into meaningful shifts in take-home pay across millions of households.

While the final number for the 8th Pay Commission is yet to be determined, discussions and early estimates suggest a broad range of 2-2.5, depending on inflation trends, negotiations, and the government’s fiscal comfort.

In practical terms, that could imply:

- A 20–30% increase in overall pay levels over the current structure

- A material upward revision in minimum basic pay from current levels

The exact outcome will depend on where the fitment factor ultimately settles. But even modest changes, applied at this scale, carry significant economic weight.

DA, Pensions, and the Compounding Effect

Beyond headline pay revisions, inflation-linked components like Dearness Allowance (DA) and Dearness Relief (DR) add another layer to this story.

Ahead of the reset, DA for central government employees is already tracking in the mid-50s as a percentage of basic pay, and could be higher by the time the 8th Commission fully kicks in — which means the post-reset progression of DA again becomes a powerful second leg of the income story.

Even incremental adjustments here can move take-home pay meaningfully, sometimes well before full commission recommendations are implemented. Pensioners, are part of this cycle too.

As salaries reset, pensions typically follow, effectively extending the income impulse deeper into semi-urban and smaller-town ecosystems where many retired employees reside.

Echoes From Past Cycles

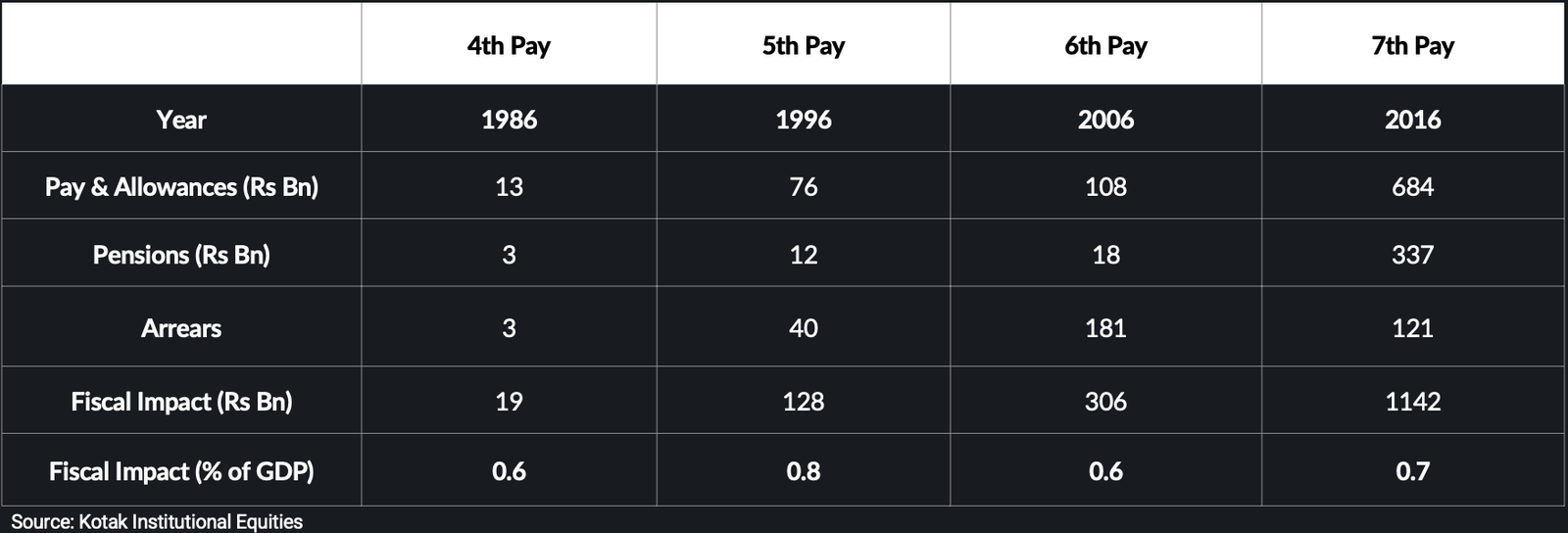

Markets have seen this before. The 7th Pay Commission, for instance, translated a 23.55% increase in overall emoluments for about 4.7 million employees and 5.2 million pensioners, lifting government wage and pension outlays and adding a visible boost to urban consumption.

The pattern was similar during the 6th Pay Commission cycle, which also coincided with a visible pickup in urban consumption.

Higher salaries translated into stronger demand for housing, automobiles, discretionary spending, and financial savings. Retailers, lenders and market observers at the time flagged a clear uptick in demand for vehicles, white goods and housing loans as arrears and higher salaries began to flow through.

Past pay cycles have added an estimated 0.6–0.8 percentage points to GDP growth through the consumption channel over a few years, depending on arrears timing and implementation.

Why This Matters Beyond Government Wallets

Most commentary treats the Pay Commission as a government employee story. That framing misses the point. The broader lens is macroeconomic.

First, consumption. A meaningful rise in incomes across millions of households tends to show up quickly in spending — homes, cars, travel, and discretionary categories. This is real demand entering the system, not stimulus created on paper.

Second, savings and capital flows. Higher take-home pay and improved pensions don’t get spent entirely. A portion consistently finds its way into bank deposits, insurance products, and market-linked assets, shaping flows across equities and long-term savings instruments.

In capital markets, previous pay cycles have coincided with stronger inflows into mutual funds, insurance and long-term savings products, as a slice of higher, more predictable income gets formalized rather than left in idle cash balances.

Third, the fiscal balancing act. Earlier commissions have pushed the Centre’s wage bill higher by around 0.6–0.8 percentage points of GDP, with the last cycle taking it close to 3% of GDP.

State finances tend to bear an even larger cumulative share once they align their pay scales. Higher wage and pension bills force trade-offs — stronger revenue mobilization, tighter non-priority spending, or acceptance of a slightly wider deficit.

The Rate Cycle Tailwind

This income reset is also landing at a supportive macro moment.

Over the past year, the Reserve Bank of India has decisively eased policy rates, with the repo rate moving from 6.5% to 5.25% as inflation moderated. Lower borrowing costs, combined with improving real incomes, tend to reinforce consumption and risk appetite.

When income certainty improves alongside easier financial conditions, households do not just spend more. They commit more. Longer EMIs feel manageable. Market-linked savings feel less intimidating. The marginal decision shifts.

What This Means for Capital

The relevance of the 8th Pay Commission. lies well beyond salary tables.

A broad-based income reset changes behaviour at the margin. It nudges savings away from idle balances. It increases comfort with long-duration commitments. It creates a steady tailwind for consumption-linked sectors and formal financial assets.

These shifts don’t arrive overnight. But they are visible, repeatable, and historically consistent.

As 2026 unfolds, this reset may prove to be one of the year’s most under-appreciated forces shaping economic sentiment — and capital flows.

Until next Sunday!

If you enjoy reading Sunday Shots — share it among your friends, family, or even strangers on WhatsApp, LinkedIn, and X.

Good insights travel best through good company.

Primary inspiration and select data points: “The Great Salary Hike: Inside the 8th Pay Commission”, Kotak Mutual Fund, December 2025.

Additional sources: Finance Ministry disclosures (Lok Sabha, December 2025), RBI Annual Report FY17, RBI policy updates, Bajaj Finserv, and other public sources.

Disclaimer: This update is for informational purposes only. Please consult a SEBI-registered advisor before investing.