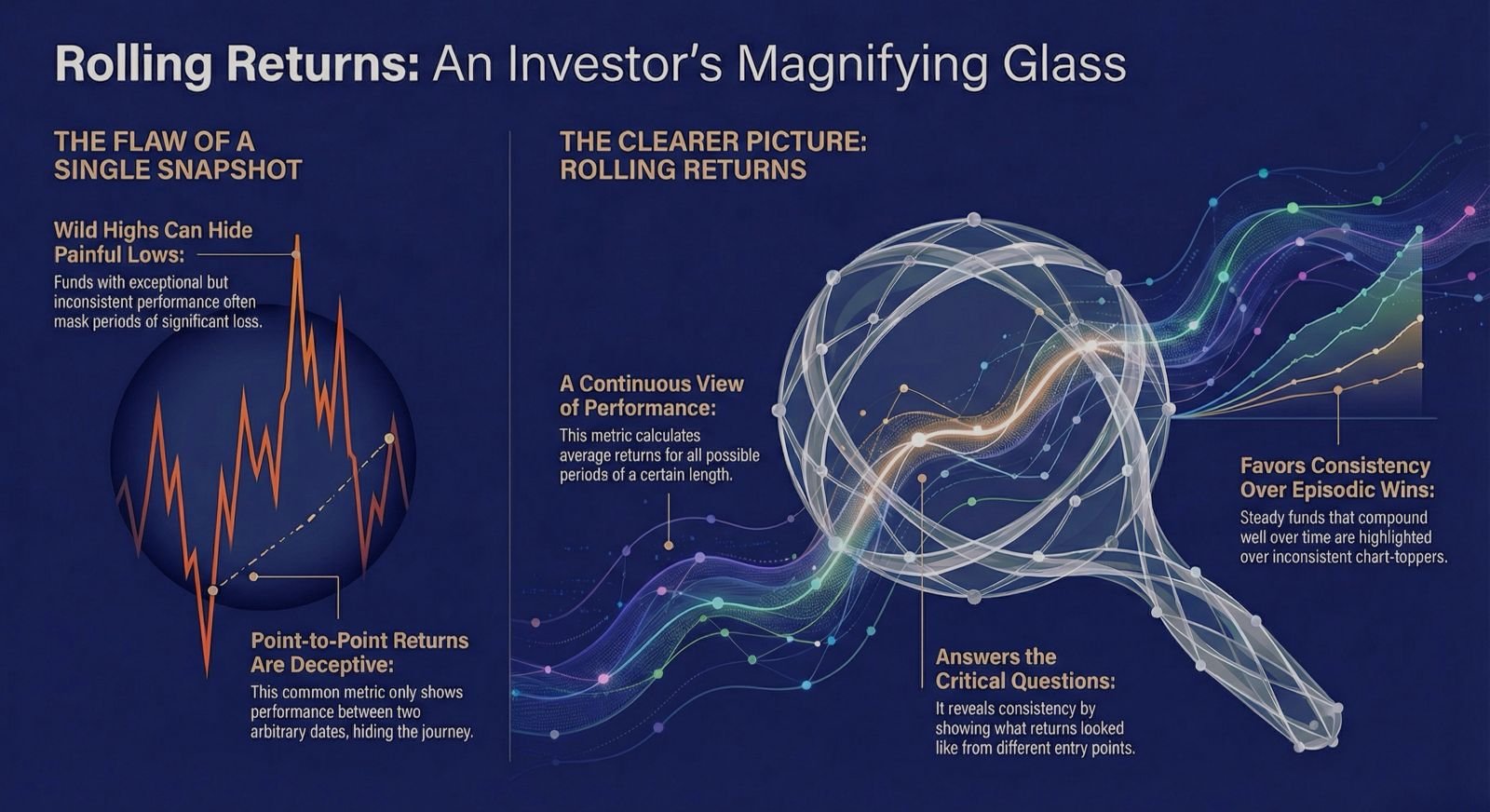

Ever opened an investing app, sorted by “1-year returns,” and felt that sense of satisfaction picking the fund at the top?

That feeling is familiar. It’s human. And it’s where things start going wrong.

Recently, Radhika Gupta, CEO of Edelweiss Mutual Fund, put a name to this behaviour: “The Sorting Investor.”

It landed because it described something most investors do, often without realizing it.

They don’t speculate. They don’t gamble. They don’t chase tips.

They simply sort and choose – by returns, by rankings, by whatever sits at the top

Clean. Logical. Efficient. It feels like how smart people should invest.

The data, however, tells a very different story.