Not always. And that’s exactly why factor investing is often misunderstood.

No single factor wins in every market.

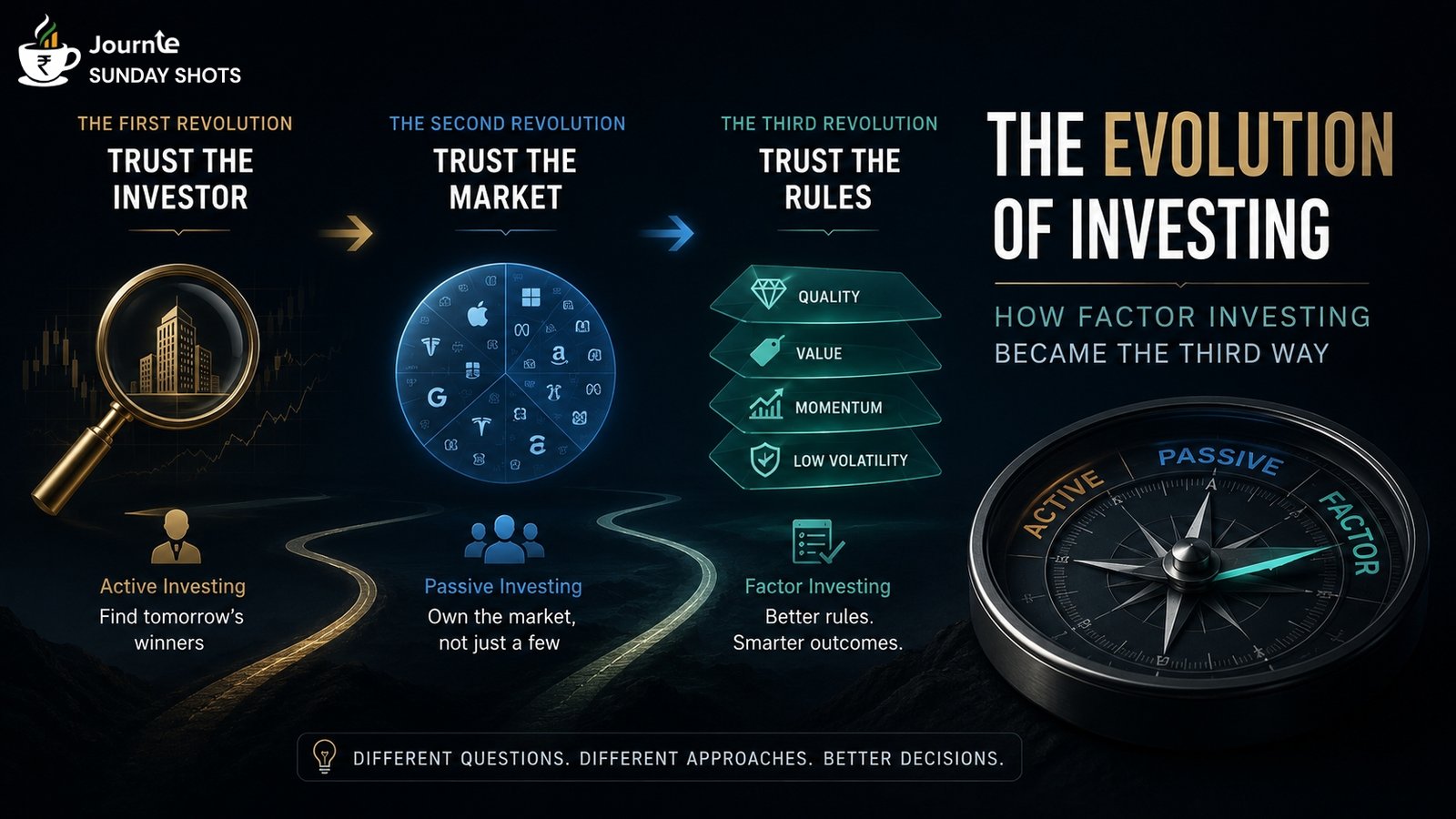

Momentum can struggle when markets suddenly reverse. Value can remain out of favour for years. Quality may underperform during speculative rallies. Low Volatility can lag during strong bull markets.

That’s because each factor is designed to capture a different characteristic of the market—not to outperform all the time.

In practice, investors rarely rely on just one factor.

Much like building a cricket team, you wouldn’t fill the entire squad with only batters or only bowlers. You’d want a balanced team where different strengths complement each other.

Portfolio construction works the same way.

Rather than relying on a single factor, many investors combine Quality, Value, Momentum and Low Volatility to create multi-factor portfolios.

The idea isn’t that one factor will always outperform, but that different factors may complement each other across different market environments — potentially improving long-term risk-adjusted returns without relying entirely on human judgement.

So perhaps the better question isn’t, “Is factor investing better?” It’s, “Better for whom—and under what conditions?”

Active investing says: Trust the manager.

Passive investing says: Trust the market.

Factor investing says: Trust the rules—but choose the rules carefully.