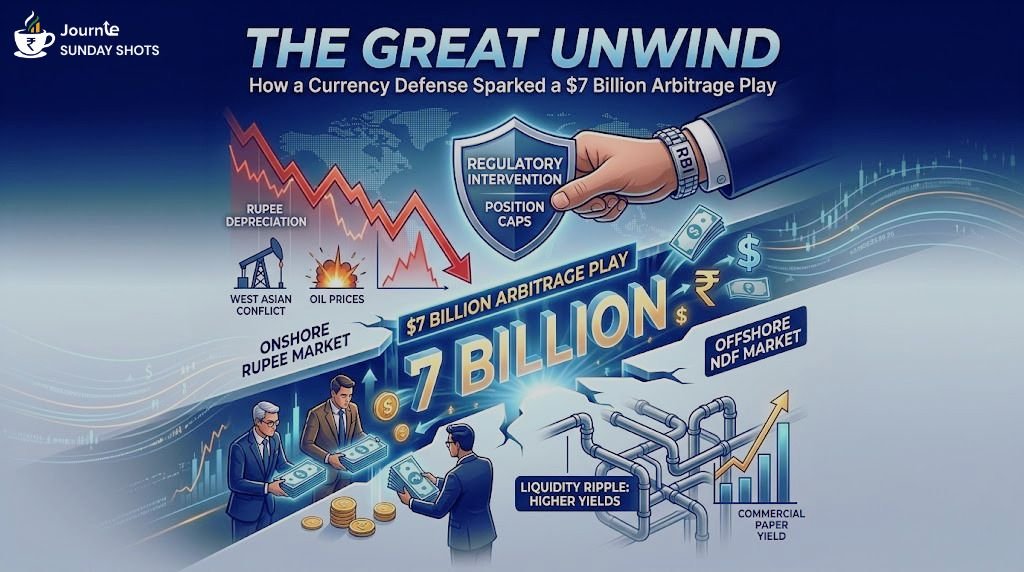

Beyond the Trade

This episode is more than a fleeting market event; it is a live case study in how regulatory shifts can temporarily distort markets.

For modern treasuries, the ability to monitor these macro cross-currents and execute true-to-label hedging strategies is no longer just a defensive necessity—it is an active driver of value.

Managing liquidity and seizing strategic arbitrage through such volatility separates the reactive from the prepared.Until next Sunday!