The post-pandemic financial system looks fundamentally different from the one that existed before 2008.

Central-bank balance sheets remain large. Capital moves across borders at unprecedented speed. Bond markets are deeper, larger, and more interconnected. Artificial Intelligence is enabling real-time treasury and liquidity management.

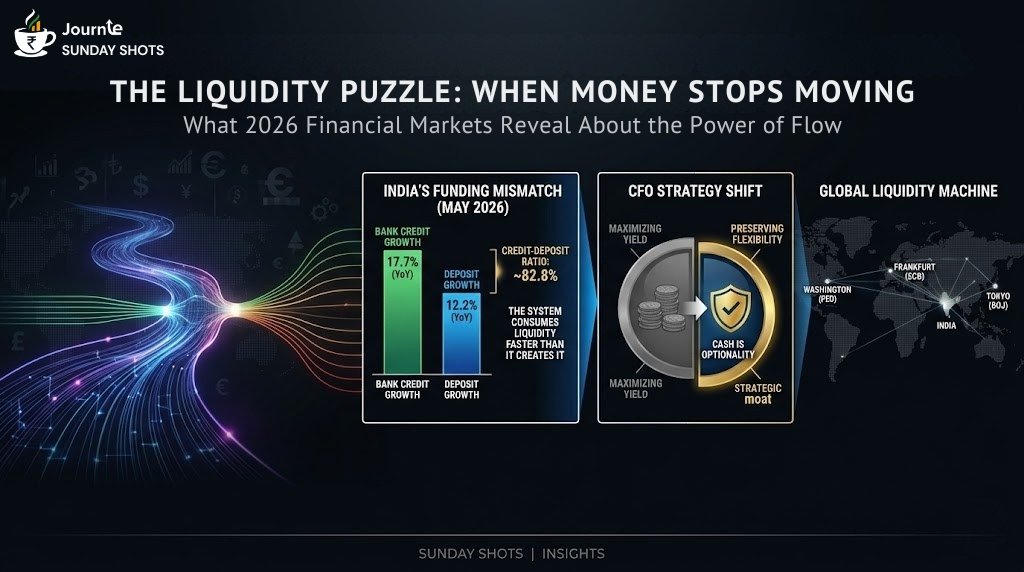

In this environment, the availability of money may matter more than its price.

Interest rates will continue to influence borrowing decisions. But liquidity will increasingly determine market resilience, financial stability, and investor confidence.

The investors who understand liquidity cycles will likely understand market cycles.

Because the defining question of the next decade may not be, "What is the interest rate?"

It may be, "Where is the liquidity flowing?"

See you next Sunday for another shot of insights!