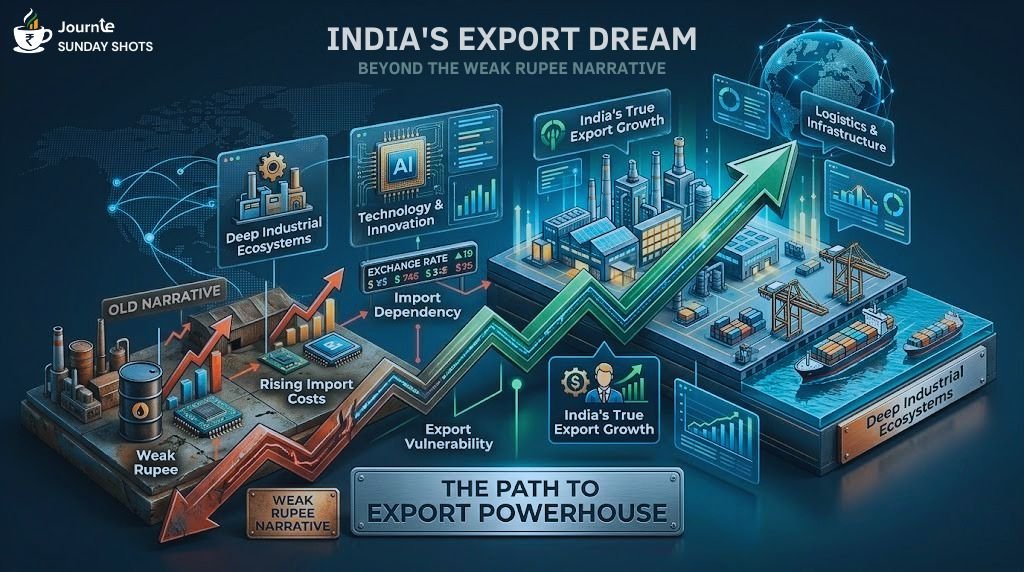

A weaker rupee may temporarily support exports by improving price competitiveness in select industries. However, durable economic strength is not built through currency depreciation alone.

The world’s leading export economies did not emerge because they had cheaper currencies. They succeeded because they developed industrial depth, technological capability, efficient logistics, integrated supply chains, and highly skilled workforces.

That remains the larger lesson often overlooked in market conversations.

India possesses the scale, strategic relevance, and economic potential to become a far more influential export economy. .

But achieving that transformation will depend less on exchange-rate movements and far more on the country’s ability to strengthen its industrial foundation in the coming decade.

See you next Sunday for another shot of insights!