The Beginning of a Different Globalization

For decades, globalization followed a simple idea: produce more, produce cheaper, and let scale do the rest.

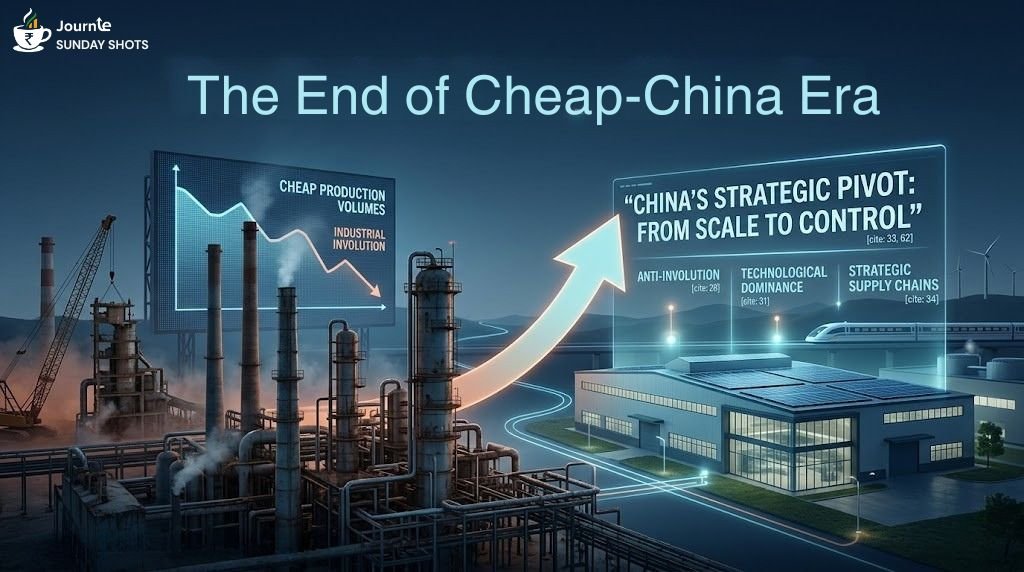

China mastered that playbook better than anyone. And now, it appears to be moving beyond it.

What is emerging instead is a more controlled version of globalization—one where output is measured, pricing is protected, and strategic sectors are carefully managed.

This is not de-globalization. It is a redesign.

And at the centre of that redesign is a subtle but important shift: China is no longer optimizing only for growth. It is optimizing for control.

See you next Sunday, for another Shot of insights.!